Most ebook files are in PDF format, so you can easily read them using various software such as Foxit Reader or directly on the Google Chrome browser.

Some ebook files are released by publishers in other formats such as .awz, .mobi, .epub, .fb2, etc. You may need to install specific software to read these formats on mobile/PC, such as Calibre.

Please read the tutorial at this link: https://ebookbell.com/faq

We offer FREE conversion to the popular formats you request; however, this may take some time. Therefore, right after payment, please email us, and we will try to provide the service as quickly as possible.

For some exceptional file formats or broken links (if any), please refrain from opening any disputes. Instead, email us first, and we will try to assist within a maximum of 6 hours.

EbookBell Team

0.0

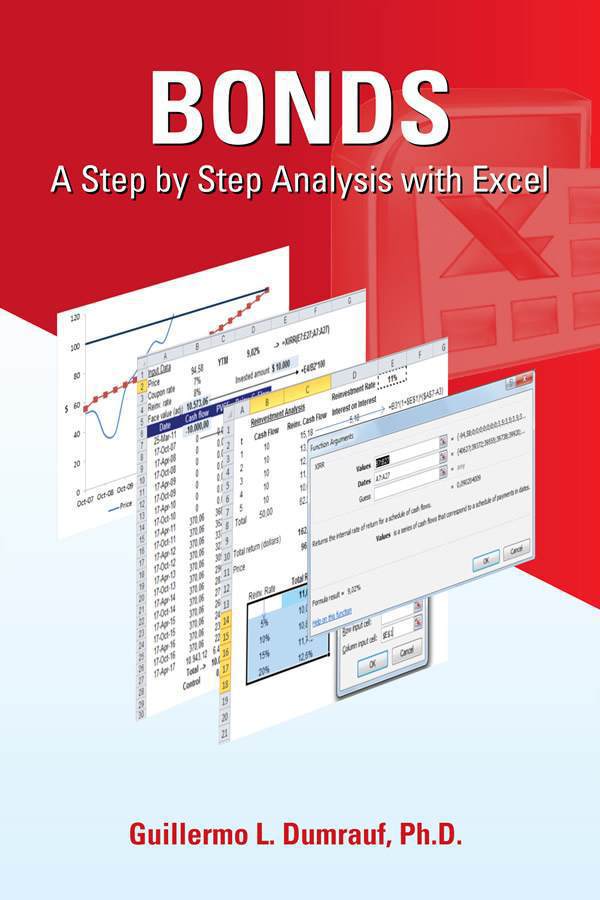

0 reviewsChapter One describes how to price a bond and calculate the different measures of return working with real bond examples and Excel spreadsheets. Beginning with hypothetical examples, we then work with a real bond, describing a step by step procedure to design the cash flow in a spreadsheet, compute the yield to maturity and other measures of return, according to the bond indenture. After reading this chapter, you will be capable of:

• Designing the cash flow for a particular investment amount

• Pricing a bond and calculating its yield to maturity, using an Excel spreadsheet.

• Calculating the total return for an investment horizon.

• Performing a sensitivity analysis of price, yield and total return.

Chapter Two describes in detail two measurements to estimate the volatility of a bond price: duration and convexity. After reading this chapter you will be capable of:

• Understanding the price-yield relationship of an option-free bond.

• Calculating the duration, modified duration and convexity for real bonds using Excel spreadsheets.

• Understanding why duration is a measure of a bond´s price sensitivity to yield changes.

• Understanding the limitations of the duration as a measure of price volatility and how the duration estimation can be adjusted for a bond´s convexity.

Chapter Three describes some real-world situations in which the yield cannot be interpreted directly. The examples discusses some important issues such as the need to equalize the amount of the investment, the calculation of the total return for a certain investment horizon and the portfolio’s return calculation with external cash flows. Also, there are anomalous situations that lead to a fictitious yield, such as the case of the bond prices that assume a strong probability of default. After reading this chapter you will be capable of:

• Understanding that the IRR is not always a good measure of the annual return.

• Identifying situations in which the yield requires an additional interpretation.

• Calculating a portfolio return, when there are deposits and withdrawals in a brokerage account.

Chapter Four describes the measure to calculate a portfolio return. After reading this chapter, you will be capable of:

• Calculating the different measures of a portfolio return, with and without external cash flows.

• Understanding their limitations, advantages and disadvantages.