Most ebook files are in PDF format, so you can easily read them using various software such as Foxit Reader or directly on the Google Chrome browser.

Some ebook files are released by publishers in other formats such as .awz, .mobi, .epub, .fb2, etc. You may need to install specific software to read these formats on mobile/PC, such as Calibre.

Please read the tutorial at this link: https://ebookbell.com/faq

We offer FREE conversion to the popular formats you request; however, this may take some time. Therefore, right after payment, please email us, and we will try to provide the service as quickly as possible.

For some exceptional file formats or broken links (if any), please refrain from opening any disputes. Instead, email us first, and we will try to assist within a maximum of 6 hours.

EbookBell Team

4.8

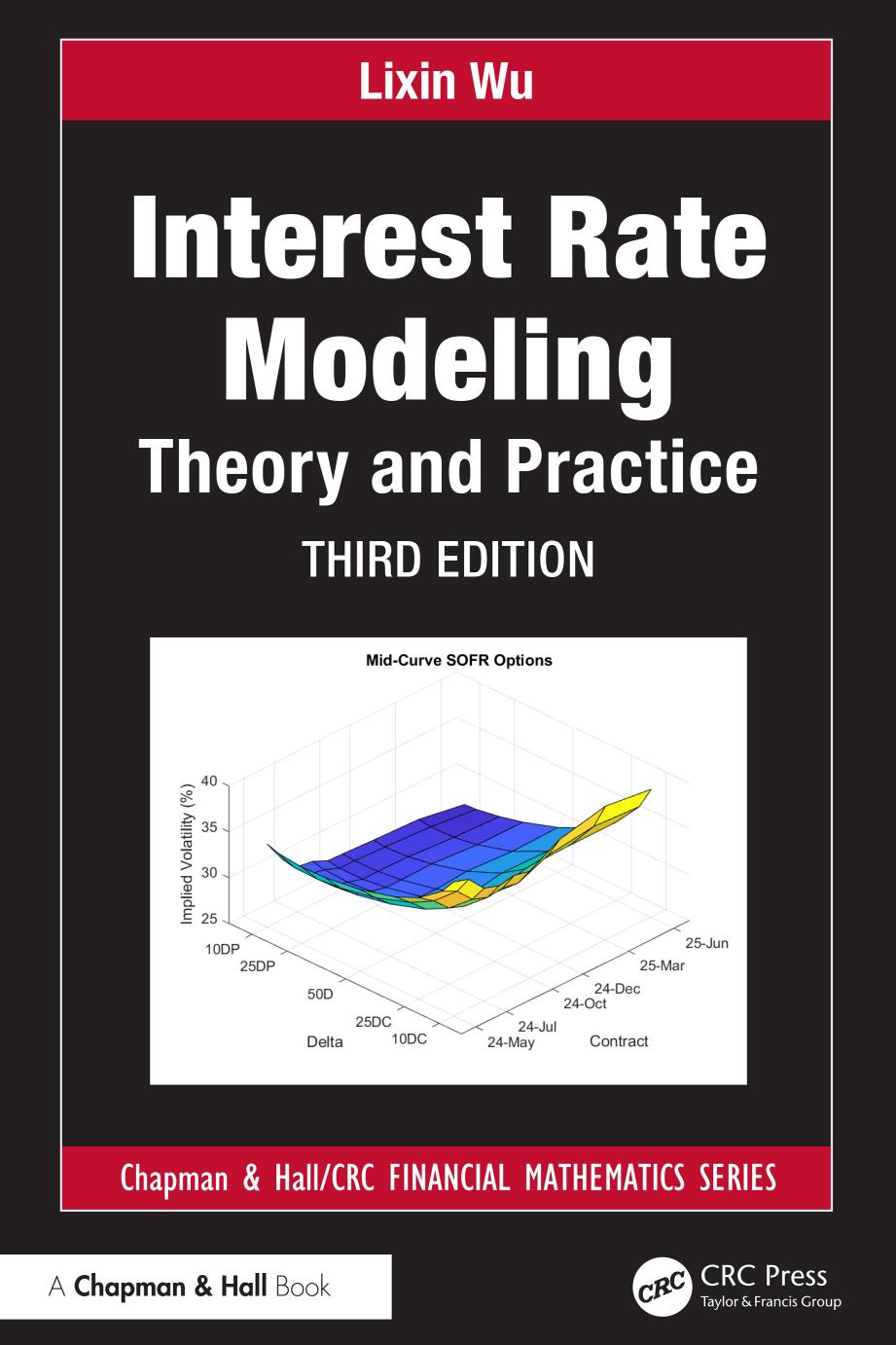

64 reviewsContaining many results that are new or exist only in recent research articles, Interest Rate Modeling: Theory and Practice portrays the theory of interest rate modeling as a three-dimensional object of finance, mathematics, and computation. It introduces all models with financial-economical justifications, develops options along the martingale approach, and handles option evaluations with precise numerical methods.

The text begins with the mathematical foundations, including Ito’s calculus and the martingale representation theorem. It then introduces bonds and bond yields, followed by the Heath–Jarrow–Morton (HJM) model, which is the framework for no-arbitrage pricing models. The next chapter focuses on when the HJM model implies a Markovian short-rate model and discusses the construction and calibration of short-rate lattice models. In the chapter on the LIBOR market model, the author presents the simplest yet most robust formula for swaption pricing in the literature. He goes on to address model calibration, an important aspect of model applications in the markets; industrial issues; and the class of affine term structure models for interest rates.

Taking a top-down approach, Interest Rate Modeling provides readers with a clear picture of this important subject by not overwhelming them with too many specific models. The text captures the interdisciplinary nature of the field and shows readers what it takes to be a competent quant in today’s market.

This book can be adopted for instructional use. For this purpose, a solutions manual is available for qualifying instructors.