Most ebook files are in PDF format, so you can easily read them using various software such as Foxit Reader or directly on the Google Chrome browser.

Some ebook files are released by publishers in other formats such as .awz, .mobi, .epub, .fb2, etc. You may need to install specific software to read these formats on mobile/PC, such as Calibre.

Please read the tutorial at this link: https://ebookbell.com/faq

We offer FREE conversion to the popular formats you request; however, this may take some time. Therefore, right after payment, please email us, and we will try to provide the service as quickly as possible.

For some exceptional file formats or broken links (if any), please refrain from opening any disputes. Instead, email us first, and we will try to assist within a maximum of 6 hours.

EbookBell Team

4.4

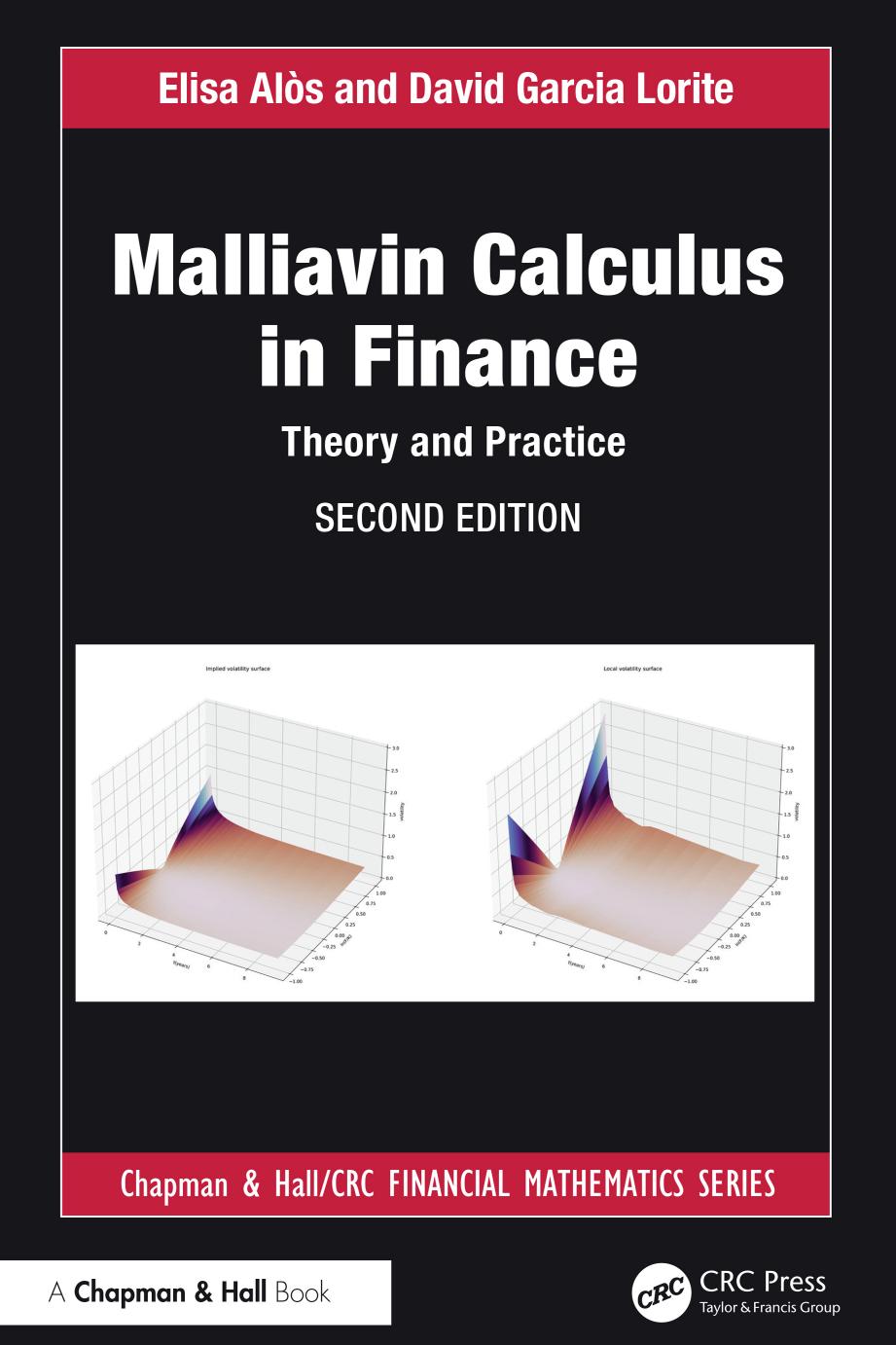

22 reviewsWhile the original works on Malliavin calculus aimed to study the smoothness of densities of solutions to stochastic differential equations, this book has another goal. It portrays the most important and innovative applications in stochastic control and finance, such as hedging in complete and incomplete markets, optimisation in the presence of asymmetric information and also pricing and sensitivity analysis. In a self-contained fashion, both the Malliavin calculus with respect to Brownian motion and general L?vy type of noise are treated.

Besides, forward integration is included and indeed extended to general L?vy processes. The forward integration is a recent development within anticipative stochastic calculus that, together with the Malliavin calculus, provides new methods for the study of insider trading problems.

To allow more flexibility in the treatment of the mathematical tools, the generalization of Malliavin calculus to the white noise framework is also discussed.

This book is a valuable resource for graduate students, lecturers in stochastic analysis and applied researchers.