Most ebook files are in PDF format, so you can easily read them using various software such as Foxit Reader or directly on the Google Chrome browser.

Some ebook files are released by publishers in other formats such as .awz, .mobi, .epub, .fb2, etc. You may need to install specific software to read these formats on mobile/PC, such as Calibre.

Please read the tutorial at this link: https://ebookbell.com/faq

We offer FREE conversion to the popular formats you request; however, this may take some time. Therefore, right after payment, please email us, and we will try to provide the service as quickly as possible.

For some exceptional file formats or broken links (if any), please refrain from opening any disputes. Instead, email us first, and we will try to assist within a maximum of 6 hours.

EbookBell Team

5.0

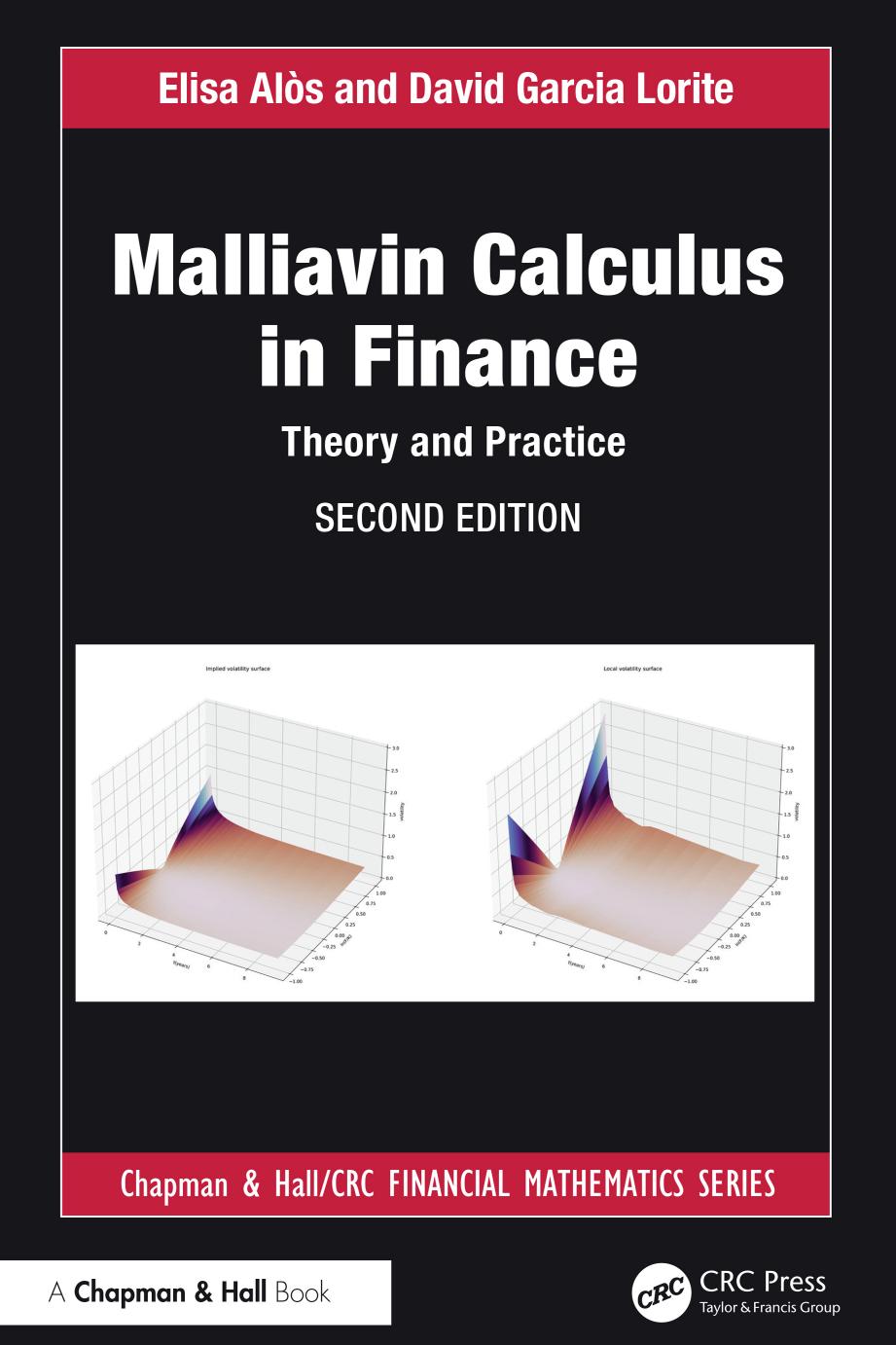

68 reviewsMalliavin Calculus in Finance: Theory and Practice aims to introduce the study of stochastic volatility (SV) models via Malliavin Calculus.

Malliavin calculus has had a profound impact on stochastic analysis. Originally motivated by the study of the existence of smooth densities of certain random variables, it has proved to be a useful tool in many other problems. In particular, it has found applications in quantitative finance, as in the computation of hedging strategies or the efficient estimation of the Greeks.

The objective of this book is to offer a bridge between theory and practice. It shows that Malliavin calculus is an easy-to-apply tool that allows us to recover, unify, and generalize several previous results in the literature on stochastic volatility modeling related to the vanilla, the forward, and the VIX implied volatility surfaces. It can be applied to local, stochastic, and also to rough volatilities (driven by a fractional Brownian motion) leading to simple and explicit results.

Features